….the path forward is clear: establish credibility (audit), protect citizens (PSIA), discipline spending (savings regime and national productive investments), fix structural constraints (energy transition), and sustain trust (compact). Skipping this sequence risks turning reform into a cycle of pain without progress. The question is no longer whether reform was necessary, but whether Nigeria will turn it into real, measurable progress and economic rebirth.

From Subsidy Removal to Debt Traps

Nigeria’s age-long fuel subsidy regimes resisted reforms, drained public finances, fuelled corruption, encouraged smuggling, and undermined local refining. Repeated reform attempts failed to resolve the underlying distortions. Jonathan’s 2012 attempt was reversed within weeks amidst ”Occupy Nigeria” protests and Buhari’s 2016 full removal was quietly reinstated under pressure. By 2022, subsidy costs surged to ₦4 trillion, with projections up to ₦17 trillion, about 77 per cent of the 2023 budget. On 29 May, 2023, President Tinubu abruptly declared “subsidy is gone”, triggering a major economic shock. With fuel underpinning 90 per cent of Nigeria’s transport and logistics, the jump in pump prices from about ₦185 to ₦617 spiked transport costs by 234 per cent, amplifying inflation to 34.2 per cent (food > 40 per cent), poverty, alongside the cost of living exacerbated, and #Endbadgovernance protest was hurriedly quelled by government in August, 2024.

President Tinubu’s decision to end fuel subsidy was widely praised for its boldness. The reform promised $7.5 billion in annual savings, $2.5 billion in new oil and gas investments, expanded infrastructure funding, cash transfers, ₦500 billion in palliatives, 3,000 CNG mass transit buses, improved gas‑powered electricity, and reinvestments into rail and other projects. These commitments were framed as a national economic rebirth within the Renewed Hope Agenda. Consequently, federation allocations rose sharply between 2023 and 2024, and they have continued climbing.

Nigeria’s economy was already fragile as at 29 May, 2023 (₦77 trillion in public debt, 22.8 per cent inflation, FX distortions, $7 billion in CBN arrears), conditions that President Tinubu described as a near-collapse. The subsidy removal without any preparation and clear reinvestments worsened these pressures, while external shocks compounded the strain. Trump’s 14 per cent tariffs weakened FX inflows and accelerated naira depreciations, while the US–Israel–Iran war pushed oil prices towards $100 per barrel, worsening energy costs, eroding real incomes, and deepening poverty.

Nearly three years on, progress has lagged. An October 2025 report by the Socio-Economic Rights Accountability Project noted that despite ₦14 trillion of subsidy savings shared across 36 states and the FCT, there has been little improvement in infrastructure or public services. At the federal level, debt servicing in the 2026 budget is projected at ₦15.52 trillion, exceeding the combined ₦14.97 trillion allocated to health, education, and security. For many Nigerians, the promised gains from subsidy removal remain distant and intangible. This piece therefore examines why Nigeria’s 2023 reform has struggled, benchmarks it against countries that applied subsidy removal as a development catalyst, and outlines practical steps to translate reform into tangible progress.

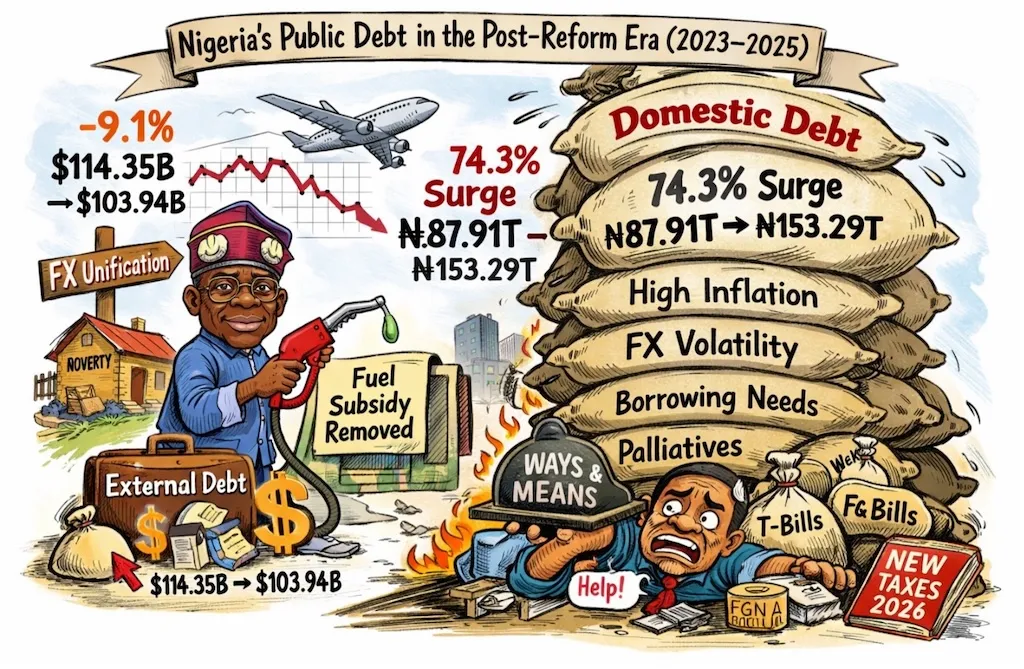

Nigeria’s Public Debt, Post‑Subsidy (2023–2025)

In June 2023, Tinubu’s administration unified multiple exchange-rate windows, triggering sharp naira depreciation, while aligning rates with market realities. Together with subsidy removal, these twin reforms reshaped Nigeria’s macro-fiscal and public debt landscape.

Between September 2023 and 2025, the total public debt amounts outstanding in $ fell by 9.1 per cent from $114.35 billion to $103.94 billion, while amounts outstanding in ₦ surged by 74.3 per cent from ₦87.91 trillion to ₦153.29 trillion – a divergence in post‑reform debt dynamics. This reflects less a sign of fiscal restraint than a valuation effect driven by sharp naira depreciation, following the exchange rate unification. In real terms, Nigeria’s debt burden has intensified, exposing rising cost and currency risks.

The surge in naira-denominated debt reflects post-reform economic pressures (high inflation, FX volatility, weak revenues, and debt-financed palliatives) driving higher spending and borrowing, rather than creating real fiscal space. Cushioning the reform shock through cash transfers and wage adjustments absorbed much of the subsidy savings. Meanwhile, limited access to concessional finance shifted borrowing towards treasury bills, FGN bonds, and Ways and Means advances. With Nigeria’s low revenue-to-GDP ratio and no transparent record of subsidy savings translating into fiscal relief, the 2025 tax reform became necessary. Crucially, the fiscal space expected from subsidy removal has not translated into fiscal discipline but it has rather reshaped it, leaving Nigeria more vulnerable to a cycle of debt accumulation.

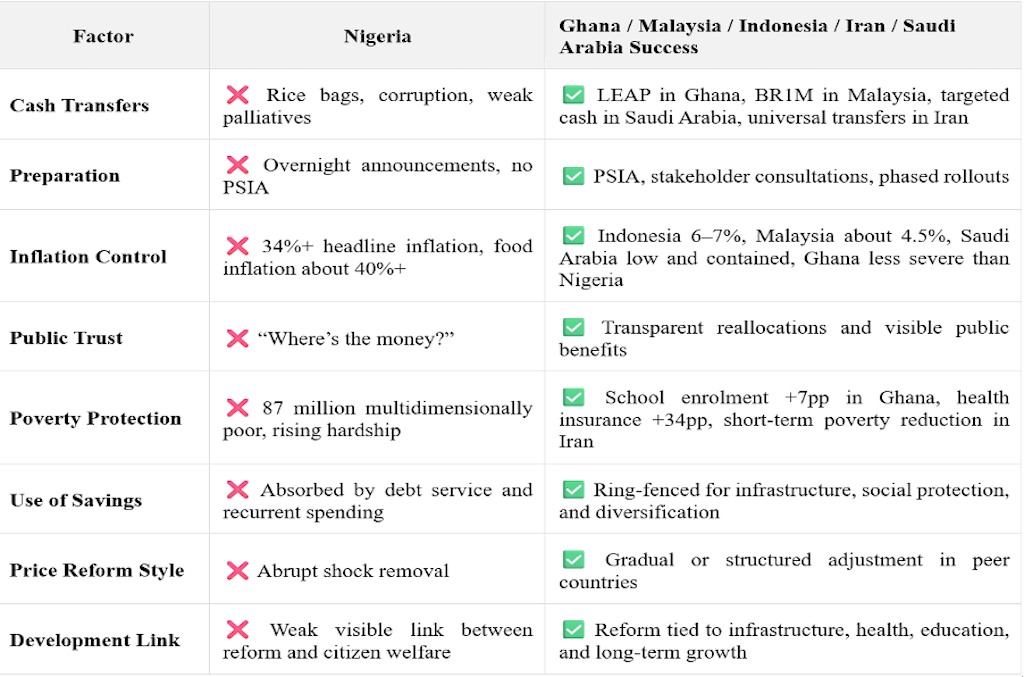

While most peer countries achieved stronger post‑subsidy reform outcomes due to effective preparation, targeted and scalable compensation, and clear reinvestment, Nigeria, by contrast, removed subsidies without an effective roadmap, rather, relying on ad‑hoc palliatives that neither cushioned the shock nor built public trust.

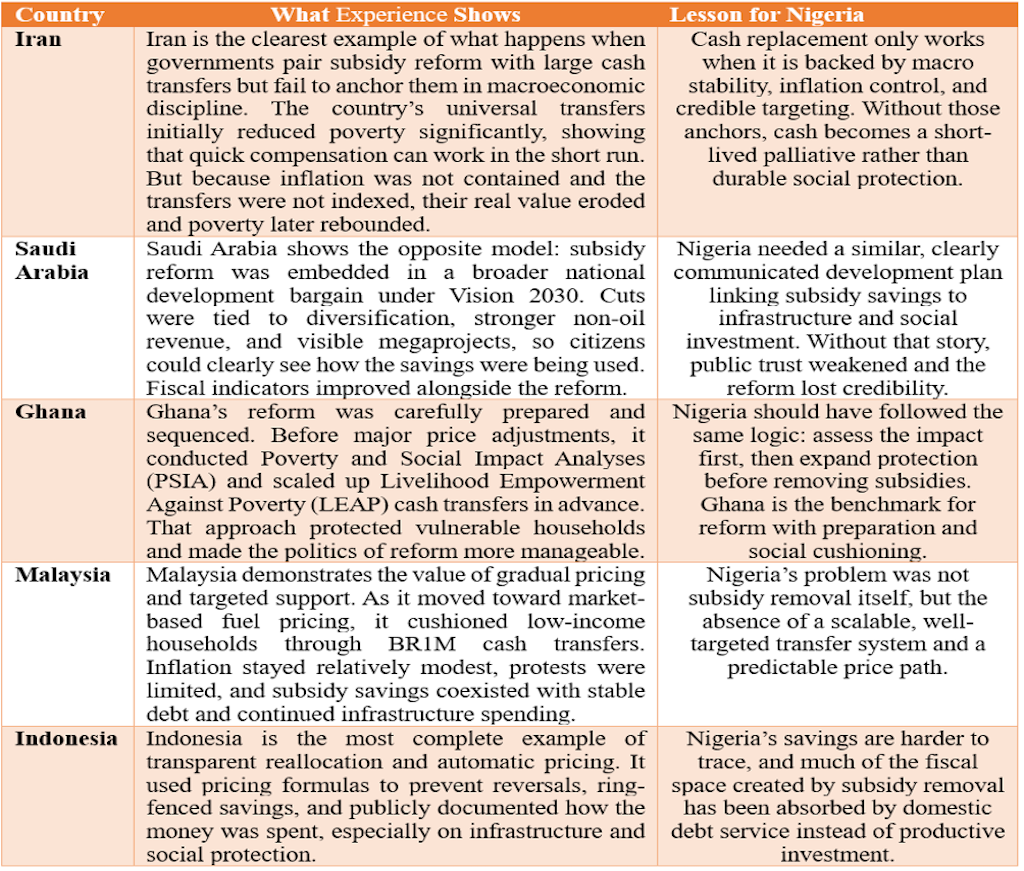

Subsidy Reforms: Nigeria vs Global Peers

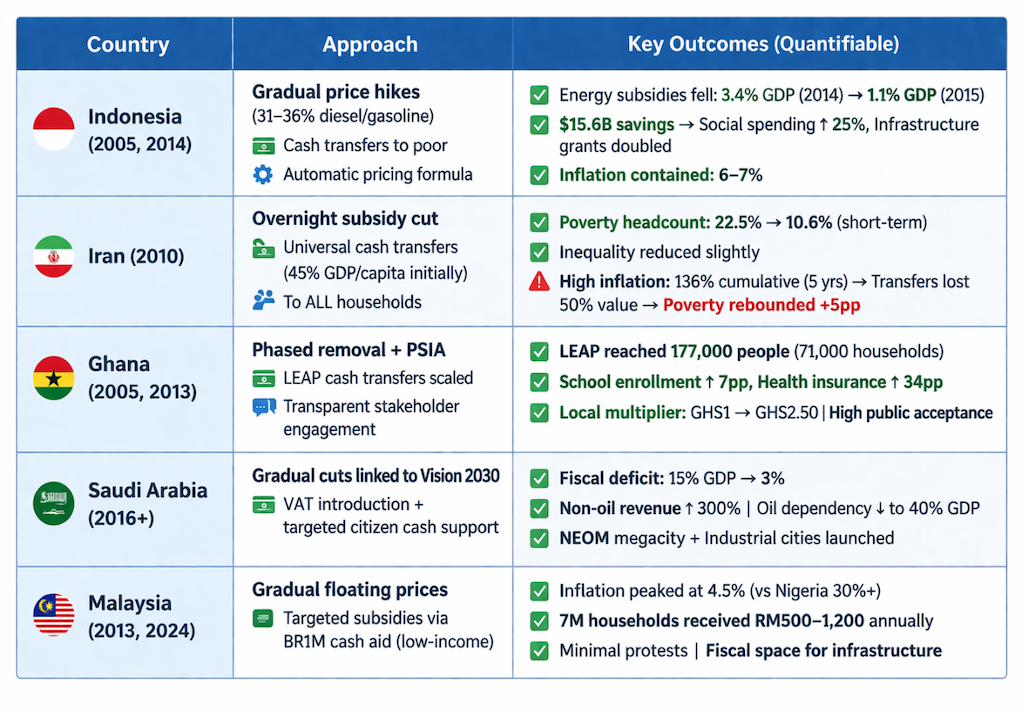

Iran, Saudi Arabia, Ghana, Malaysia, and Indonesia are resource-rich, emerging or middle-income economies that once sustained large subsidies, and faced similar fiscal pressures around energy subsidies like Nigeria.

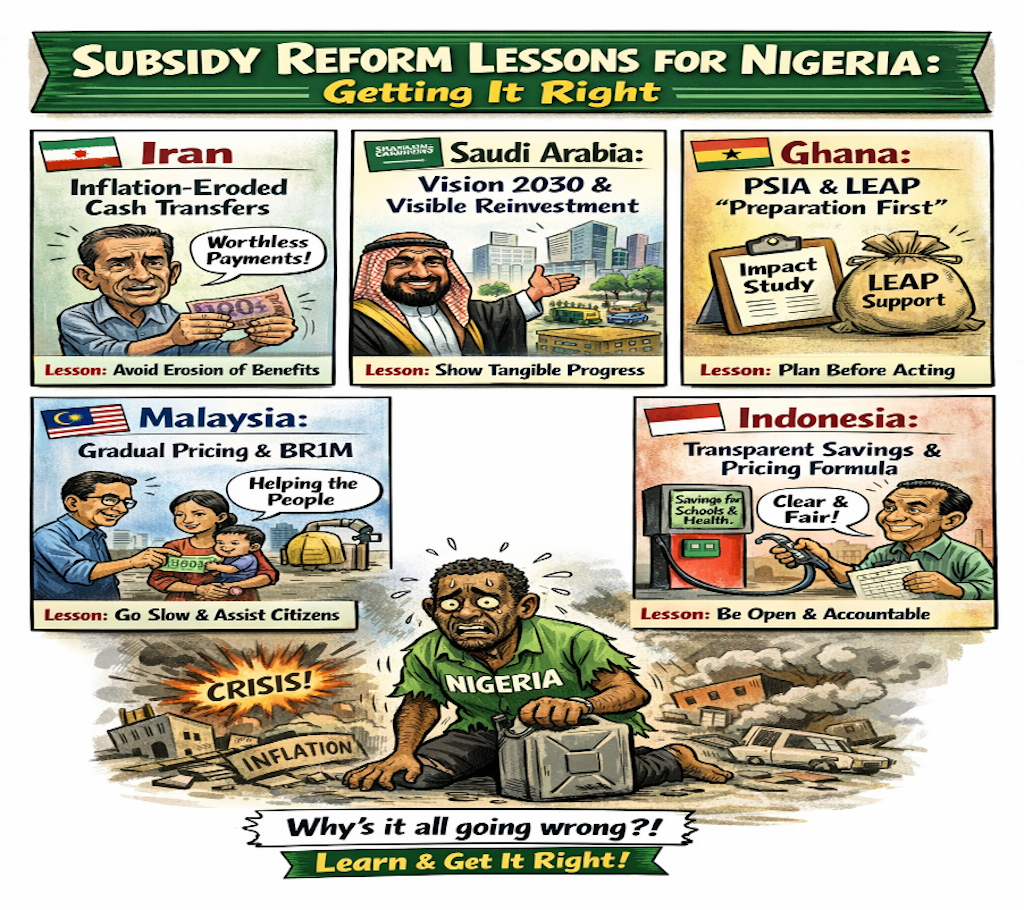

Indonesia phased fuel price hikes, and cut energy subsidies from 3.4 per cent of GDP in 2014 to 1.1 per cent in 2015. Iran’s overnight removal briefly reduced poverty before inflation eroded the gains in five years. Ghana used Poverty and Social Impact Analysis and expanded Livelihood Empowerment Against Poverty (LEAP) as a cushion to households. Saudi Arabia tied gradual cuts to Vision 2030, targeted cash support, and large-scale industrial development, including the NEOM megacity. Malaysia floated prices gradually, while protecting low‑income households and preserving the fiscal space.

Across these cases, governments paired subsidy reform with measures that protected households, contained inflation, strengthened social spending, expanded infrastructure, and improved fiscal stability.

While most peer countries achieved stronger post‑subsidy reform outcomes due to effective preparation, targeted and scalable compensation, and clear reinvestment, Nigeria, by contrast, removed subsidies without an effective roadmap, rather, relying on ad‑hoc palliatives that neither cushioned the shock nor built public trust.

Indonesia stabilised inflation and protected growth; Ghana strengthened social protection; Malaysia kept inflation low while preserving fiscal space; Saudi Arabia deficits cut expanded non‑oil revenues; and even Iran, despite later shocks, began with a coherent design.

Nigeria’s trajectory has been far more fragile, abrupt and imposed on a far larger, poorer population than many peers. Growth remains weak, poverty is rising, and social pressures are intensifying. With limited fiscal space and governance weaknesses, and the absence of a reinvestment strategy, public debt is climbing, while savings remain largely unaccounted.

Nigeria should, within three to six months, institutionalise a “Subsidy Savings Regime,” ring-fencing and transparently allocating savings (e.g. 60 per cent to infrastructure, 25 per cent to social sectors, and 15 per cent to power), rather than redistributing through FAAC backed by public reporting to enhance reform outcomes and tracking. Otherwise, savings will dissipate into untracked spending, while debt and public disbelief worsen.

Effective subsidy reform depends not just on the right policies, but on the essential pillars of preparation, protection, purpose, sequencing and timing, approaches that deepen credibility, stabilisation, institutionalised and structural transformations.

Recommendations/Conclusion

The immediate priority is a 90-day independent audit of subsidy and FX reform savings to restore fiscal transparency, curb leakages, and rebuild public confidence. Without foundational clarity on the scale of savings, government cannot effectively reinvest. Without this, savings and reinvestments will remain opaque.

Nigeria should urgently conduct a Poverty and Social Impact Analysis (PSIA) to guide and scale targeted social protection. As seen in the US, strategic sectors like agriculture receive targeted fuel support. LEAP-style support stabilises vulnerable households and sustain consumption, thus relief must be focused and sustained. In spite of this, poverty will deepen, thereby weakening recovery.

Nigeria should, within three to six months, institutionalise a “Subsidy Savings Regime,” ring-fencing and transparently allocating savings (e.g. 60 per cent to infrastructure, 25 per cent to social sectors, and 15 per cent to power), rather than redistributing through FAAC backed by public reporting to enhance reform outcomes and tracking. Otherwise, savings will dissipate into untracked spending, while debt and public disbelief worsen.

Nigeria must accelerate investment and transition to CNG and renewable energy to reduce petrol dependence, lower transport costs, ease inflation, and create jobs. Delaying this structural shift will prolong exposure to fuel price shocks and sustain inflationary pressures.

Finally, government must rebuild trust and secure long-term buy-in of labour, CSOs and the private sector by establishing a National Economic Compact within three to six months. This compact aligns actors around measurable reform outcomes. Without this, reforms risk resistance and reversal.

In conclusion, the path forward is clear: establish credibility (audit), protect citizens (PSIA), discipline spending (savings regime and national productive investments), fix structural constraints (energy transition), and sustain trust (compact). Skipping this sequence risks turning reform into a cycle of pain without progress. The question is no longer whether reform was necessary, but whether Nigeria will turn it into real, measurable progress and economic rebirth.

David Okelue Ugwunta, a public policy and economic planning specialist, is a senior adviser (Economic) with Thoughts and Mace Advisory.